BJC bioCapital Connections

periodic musings about the biopharma industry

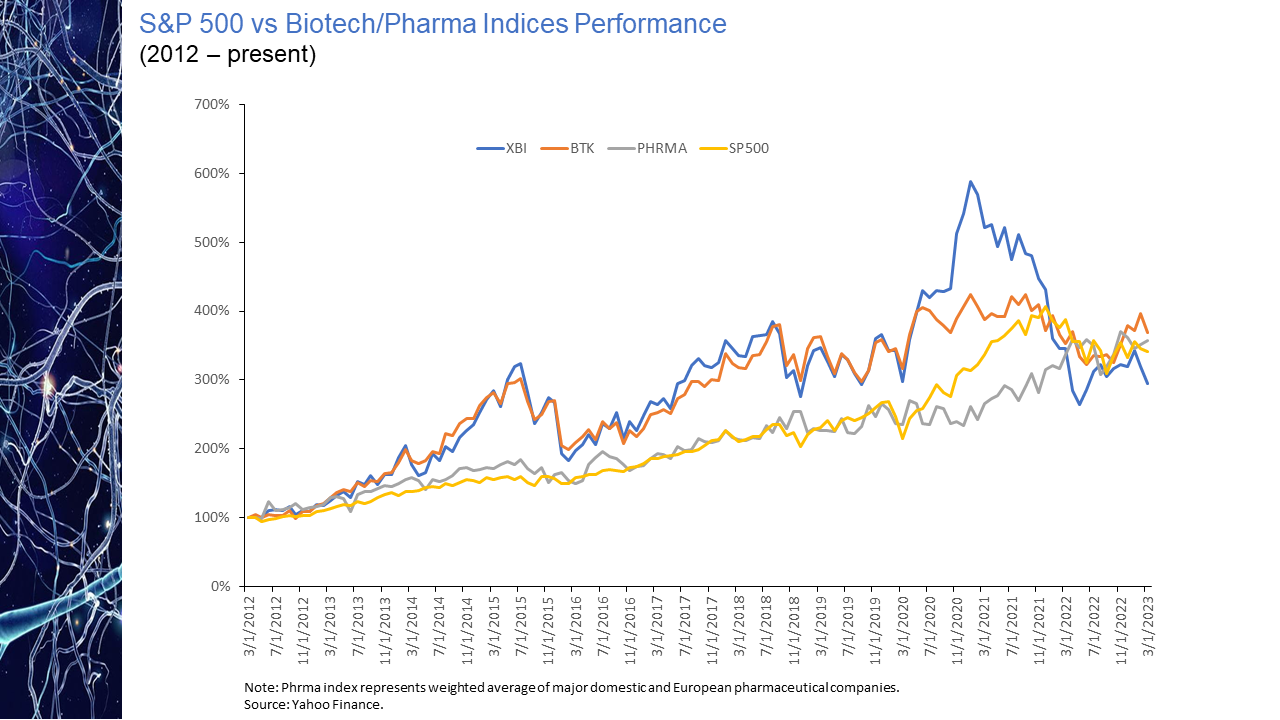

We are pleased to announce that last week we received notification from FINRA that our application for membership has been approved. Approval of the application, the culmination of a nearly ten-month process, formally designates the firm as a registered broker/dealer allowing us to participate in regulated securities transactions. FINRA membership extends the services we are able to provide earlier-stage life science companies to include private equity placements and transaction advisory services, including licensing, strategic partnerships and alliances, and mergers & acquisitions engagements, where we participate on both buy-side and sell-side engagements. These capabilities build upon decades of prior investment banking, strategy consulting and corporate management experience. Differentiating our transaction business are a range of complementary services that tailored primarily to the needs of emerging stage biopharmaceutical companies, including a chief medical officer (CMO) and chief business officer (CBO) executive network that provides access to distinguished senior-level talent on an interim or fractional basis and our IPO preparation services, where we work closely with company management to draft a compelling and thoughtful business section for S-1, F-1 and certain S-4 filings. We believe the seamless integration of this suite of capabilities addresses needs central to our clients’ success. member FINRA/SIPC The ongoing shift over the last decade towards biopharma as the primary originator of industry innovation, and the disproportionate value it generated, is perhaps best reflected in the market performance of the biopharma sector when compared to that of traditional pharmaceutical companies. As is noted in the chart presented below, over the last decade, the cumulative advance of biopharma, in particular the increase in the XBI index of earlier-stage biopharma companies, far outpaced the gains achieved by the traditional pharmaceutical industry. Remarkably, the spread in cumulative market appreciation between the XBI and traditional pharma approached an astounding 300% at its peak in early 2021.  That contrast in market appreciation, achieved over a nearly ten-year period, quickly vanished in the year that followed. The perception of R&D as a key valuation driver during a time of relatively inexpensive money, appears to have quickly reversed itself, with the cumulative gains of a decade evaporating virtually overnight. Perhaps in anticipation of the higher interest rate environment that we now find ourselves in, sentiment began to shift even before the first interest rate hike. This valuation reset has reduced the aggregate returns of the XBI to below those of traditional pharma for the first time in ten+ years. While the implications of that reset are likely to reverberate until further economic clarity is achieved, interest rate stability may usher in renewed sector advance.

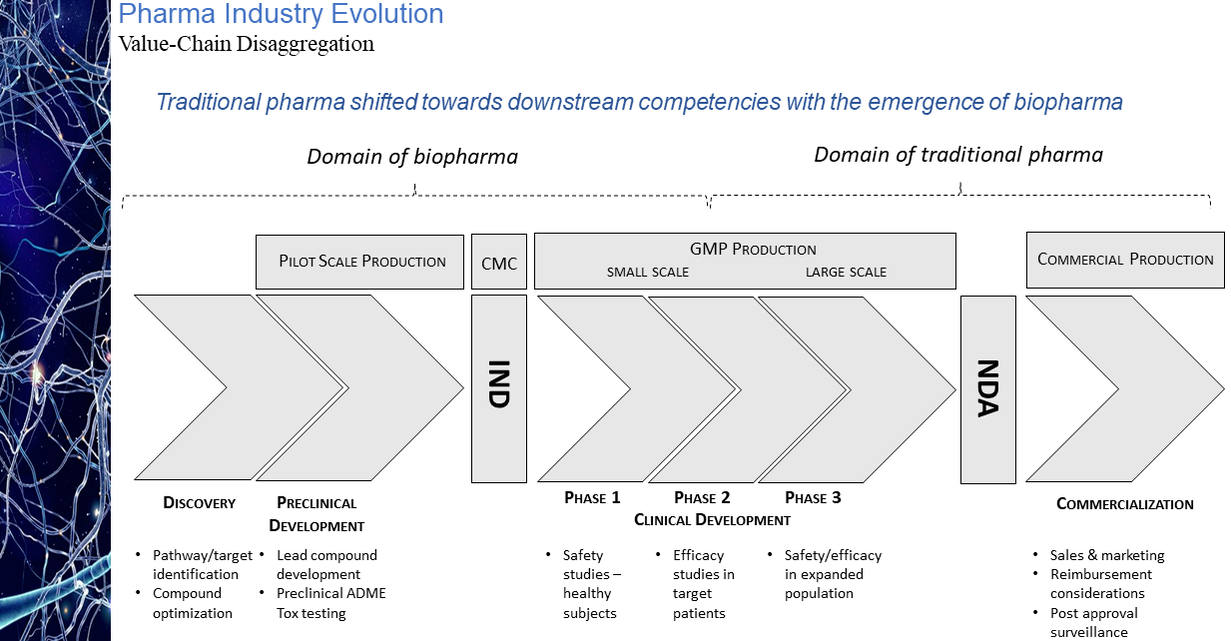

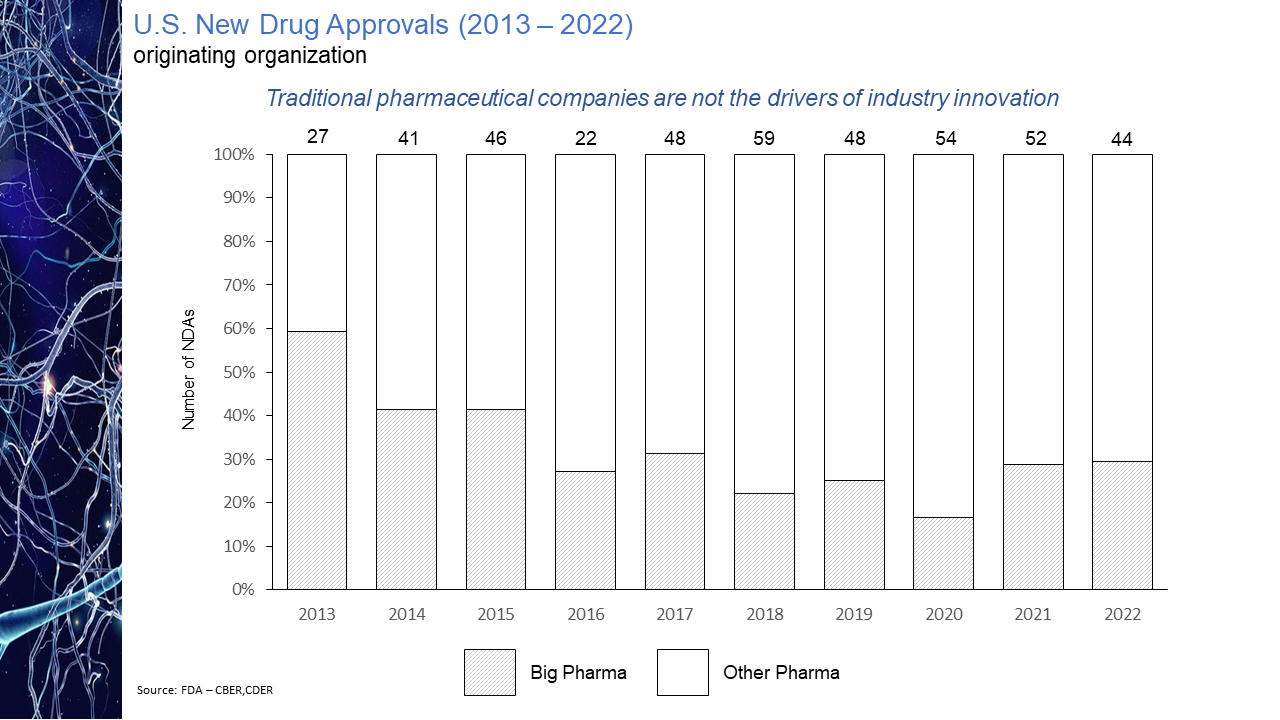

The evolution of the pharmaceutical industry has witnessed the continued disaggregation of the industry value chain. This disaggregation has resulted in larger, more established companies increasingly focused on downstream competencies in such areas as regulatory affairs and product commercialization with earlier-stage sector participants asserting themselves as the primary engines of industry innovation. As a result, today’s biopharmaceutical industry may arguably be considered largely an outsourced R&D function and feeder system for the commercial infrastructure of big pharma.  While the migration of the industry towards this functional segregation is not a new phenomenon, what is striking is the degree of the shift. As is illustrated in the chart presented below, as recently as ten years ago some 60% of novel drug approvals were tied to companies whose origins could be traced to the traditional pharmaceutical industry. Within the last handful of years, however, that percentage has dropped to as low as 20%. Even this percentage may be an overstatement of the actual figure after factoring in the acquisition appetite of big pharma for its smaller biotech peers. The implications of this shift on market performance, a topic to be explored in an upcoming blog post, is notable.  |

About the AuthorBen Conway is a long-tenured investment banker with a primary focus on the biopharmaceutical sector. In addition to investment banking, his experience includes positions in large pharma as well as with smaller emerging biotech platforms. Archives

February 2024

|

RSS Feed

RSS Feed